The previous articles traced five extensions of PayoutBase:

InterestRatePayout(scheduled)CreditDefaultPayout(contingent)OptionPayout(conditional)SettlementPayout(deterministic)- and

PerformancePayout(performance-based).

This article covers the sixth: AssetPayout (collateral-based).

At its core, AssetPayout models the movement of securities against cash — a repo, a reverse repo, a securities lending transaction, a buy/sell-back. Where every other payout type is about cash flows, AssetPayout is about asset flows. Securities go out. Securities come back. The cash leg is modelled separately.

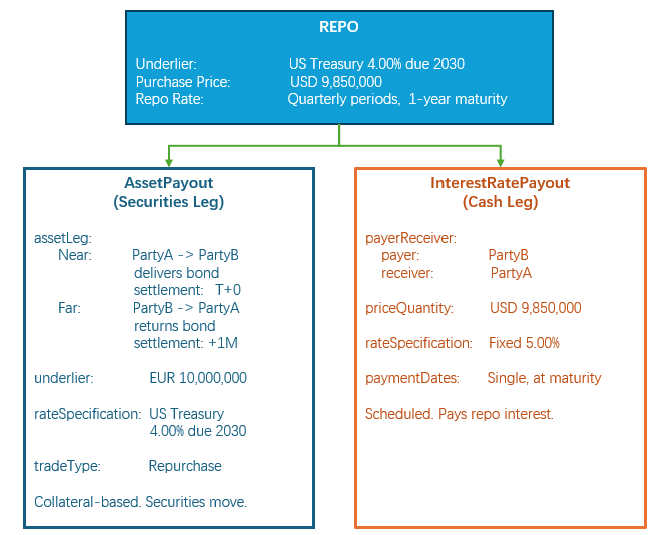

A classic repo on a US Treasury bond will serve as the running example: Party A sells USD 10,000,000 face value of the US Treasury 4.00% due 2030 to Party B for USD 9,850,000, agreeing to repurchase equivalent securities in one month at USD 9,850,000 plus repo interest at 5.00%.

The Shape of the Product

A repo, like a CDS or an equity swap, is two payouts of different types. One is an AssetPayout — the securities movement. The other is an InterestRatePayout — the repo interest on the cash.

AssetPayout — The Type Structure

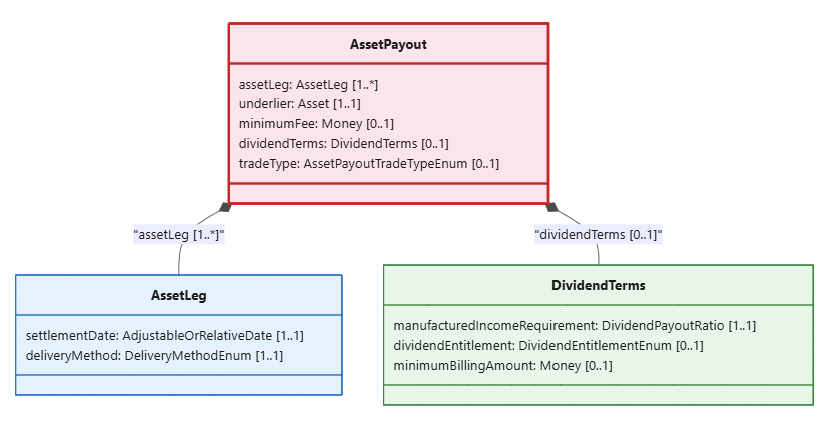

type AssetPayout extends PayoutBase: assetLeg AssetLeg (1..*) underlier Asset (1..1) minimumFee Money (0..1) dividendTerms DividendTerms (0..1) tradeType AssetPayoutTradeTypeEnum (0..1)

Five direct attributes, plus everything inherited from PayoutBase. The type surface is small — second only to SettlementPayout — because the economics are fundamentally about movement, not calculation.

assetLeg is mandatory and repeatable (1..*). It defines each movement of the security. A classic repo has two legs — near and far. An open repo may have more as the transaction rolls. Each leg carries settlementDate (when delivery occurs) and deliveryMethod (free of payment, delivery versus payment). The legs define the securities flow: Party A delivers to Party B on the purchase date; Party B returns equivalent securities on the repurchase date.

underlier is mandatory (1..1). It is the security being financed — a bond, an equity, a fund unit. The CDM enforces one constraint: the underlier cannot be Cash. This is because the cash leg is modelled separately as an InterestRatePayout. AssetPayout handles the securities. InterestRatePayout handles the interest. They are separate payouts with different types because they represent different economic obligations.

tradeType classifies the transaction: Repurchase (classic repo under GMRA), BuySellBack (economically similar, legally a pair of outright trades), or SecuritiesLending (under GMSLA, where the fee is explicit rather than embedded in a price difference).

dividendTerms defines what happens to income paid by the security during the loan. The manufacturedIncomeRequirement specifies what proportion of the dividend or coupon the borrower must return to the lender — typically 100%, expressed as DividendPayoutRatio { totalRatio: 1.00 }. The economic owner of the security should receive the same income as if the security had never been lent. dividendEntitlement defines the cutoff date — who is entitled to a dividend that falls during the loan period. minimumBillingAmount sets a floor below which fee payments are accumulated rather than settled individually.

minimumFee is a floor on the fee the borrower pays, regardless of loan duration. If the repo rate times the term produces less than the minimum, the minimum applies. This protects the lender in very short-dated transactions where the administrative cost of processing a tiny fee exceeds the fee itself.

Product Examples

AssetPayout appears wherever securities are financed — borrowed, lent, or used as collateral.

Classic repo. Party A sells a US Treasury bond to Party B for USD 9,850,000, agreeing to repurchase it in one month at the same price plus repo interest at 5.00%. The near leg delivers the bond from A to B on T+0. The far leg returns it from B to A in one month. The InterestRatePayout captures the repo interest — USD 9,850,000 × 5.00% × 30/360. The AssetPayout captures the two securities movements. tradeType = Repurchase.

Reverse repo. The same transaction from Party B’s perspective. Party B buys the bond from Party A for USD 9,850,000, agreeing to sell it back in one month plus interest. The securities flow is the same (near leg A→B, far leg B→A). The interest flow direction reverses. The model handles this through the PayerReceiver on the InterestRatePayout — Party A pays in a repo, Party B pays in a reverse repo. The AssetPayout structure is identical.

Buy/sell-back. Economically equivalent to a repo, but legally structured as two separate outright trades — a spot sale and a forward repurchase. The AssetPayout still captures the two securities movements. The price difference between the spot sale and the forward repurchase embeds the implied interest. tradeType = BuySellBack.

Securities lending. Party A lends 100,000 shares of Finsight Tech Corp to Party B. Party B pays a lending fee (modelled as an InterestRatePayout) and must return equivalent shares on demand or at term. If Finsight pays a dividend during the loan, Party B must manufacture the dividend — pay Party A the same amount. tradeType = SecuritiesLending. dividendTerms.manufacturedIncomeRequirement.totalRatio = 1.00. The legal agreement is GMSLA rather than GMRA.

Tri-party repo. Same as a classic repo, but a tri-party agent (typically a custodian bank) manages the collateral allocation, substitution, and valuation. The AssetPayout structure is the same. The tri-party mechanics are operational, not structural — the CDM models them in the collateral agreement layer, not the payout layer.

Economic Agreement — What Moves, and When?

Every other payout type starts from a cash obligation. AssetPayout starts from an asset.

The underlier is the security. The assetLeg defines the two movements: delivery and return. The tradeType defines the legal form. The direction of the cash — who pays repo interest to whom — is determined by the InterestRatePayout on the other leg. The AssetPayout only concerns itself with the securities.

This is a different kind of economic agreement. In an IRS, both parties are obligated to make payments. In a repo, one party delivers securities and receives cash at the start, then returns cash and receives securities at the end. The obligation is not to pay, but to deliver and return.

Contractual Definition — The Near and Far Legs

AssetPayout has no CalculationPeriodDates, no PaymentDates, no ResetDates. Instead it has assetLeg — a different kind of time structure tailored to delivery rather than accrual.

The near leg settles on the purchase date (typically T+0 or T+1). The far leg settles on the repurchase date (typically T+N, where N is the term of the repo). Each leg carries its own settlementDate and deliveryMethod.

For a repo, the near leg is Delivery Versus Payment — the securities and the cash move simultaneously. The far leg is also DVP. For securities lending, delivery may be Free of Payment if the collateral is held separately.

The two legs are not a schedule of recurring payments. They are a pair — out and back. The repeatable cardinality (1..*) on assetLeg accommodates open repos and structures with interim partial returns, but the base case is two.

Value Determination — No Calculation Needed

Value determination for AssetPayout is the simplest of all six types. There is nothing to calculate. The security is identified. The quantity is fixed. The settlement dates are known. The interest on the cash leg is calculated by the InterestRatePayout using the same formulaic chain we traced in articles 9–11. The AssetPayout does not produce a number. It produces a delivery instruction.

This is the cleanest separation of concerns in the CDM. The securities leg handles what moves. The cash leg handles what is paid. Neither duplicates the other. Neither tries to handle both.

Settlement / Realisation — Delivery and Return

AssetPayout inherits settlementTerms from PayoutBase, which carries the settlement method. For a repo, settlement is physical — the securities actually move. For some structured products, settlement may be cash — the difference between the agreed price and the market price is paid.

The deliveryMethod on each assetLeg specifies the operational mechanics: DVP (Delivery Versus Payment — securities and cash move simultaneously), FOP (Free of Payment — securities move without a corresponding cash movement), or Delivery Versus Delivery (two securities legs move against each other).

Conclusion

AssetPayout completes the set. Six extensions of PayoutBase, six economic natures:

| Payout type | Economic logic | What it contributes to a product |

|---|---|---|

InterestRatePayout | Scheduled | Payment based on a rate over time |

CreditDefaultPayout | Contingent | Payment triggered by a credit event |

OptionPayout | Conditional | Right to exercise at a strike |

SettlementPayout | Deterministic | Forward exchange at a fixed price |

PerformancePayout | Performance-based | Payment driven by market performance |

AssetPayout | Collateral-based | Securities delivery and return |

Five of the six are about cash. AssetPayout is about assets. It exists because securities financing transactions cannot be adequately modelled by a cash-only type. The securities movement is the point — the cash leg is the accessory. The CDM models both, separately, with each type doing what it is designed for.

The product is the composition. The label is just the label.