The previous article introduced the business meaning of OptionPayout — a conditional right attached to anything, appearing in three structural roles across products.

This article walks through the type structure itself: the attributes, how they map to the four stages of F-PAL framework, and how they differ from the InterestRatePayout and CreditDefaultPayout structures we have already seen.

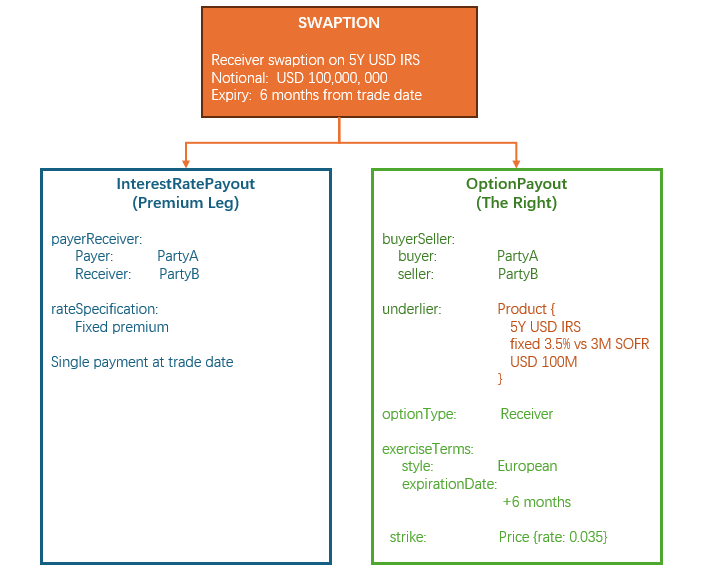

A receiver swaption on a 5-year USD IRS will serve as the running example: the buyer pays a premium for the right to enter into a swap in six months, receiving fixed 3.50% and paying 3M SOFR, on a notional of USD 100M.

Unlike a CDS, where the two legs are different types (IRP + CDP), a swaption has a simpler structure. The option premium itself may be modelled as a separate InterestRatePayout or SettlementPayout. The OptionPayout carries the right.

OptionPayout — The Type Structure

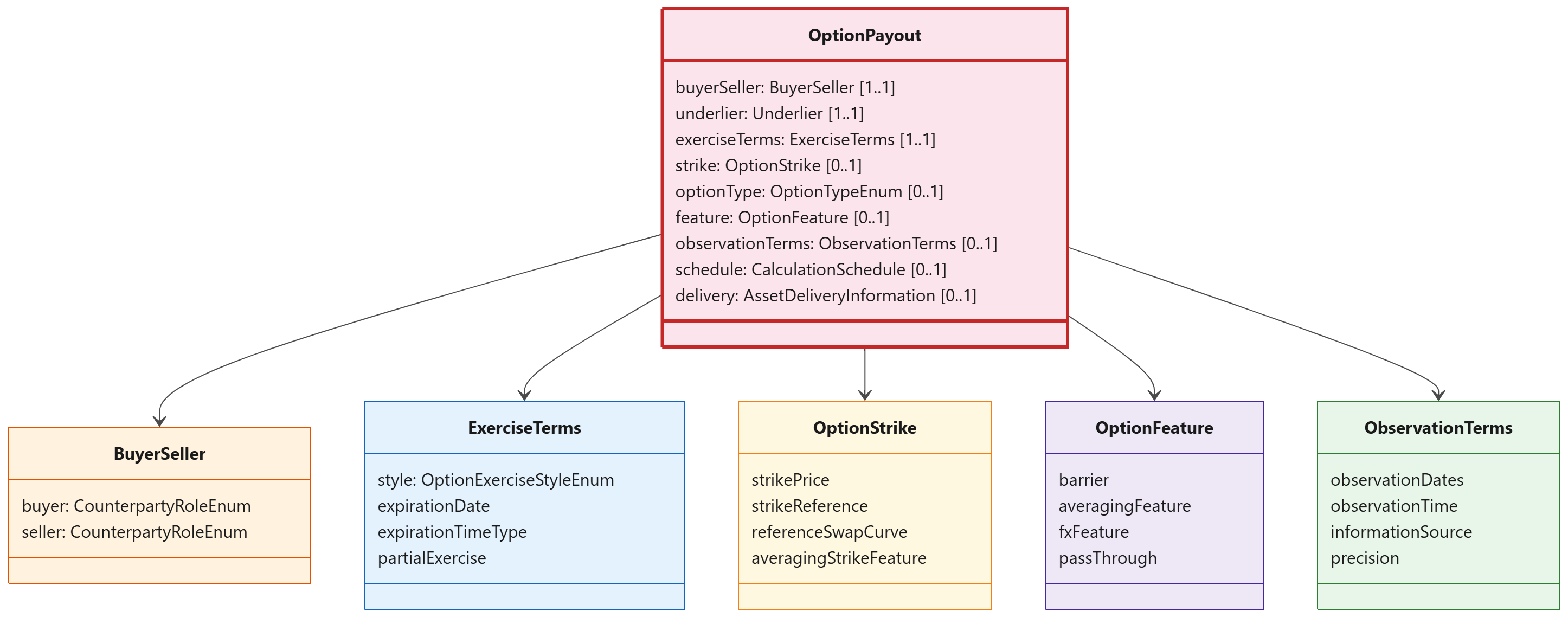

type OptionPayout extends PayoutBase: buyerSeller BuyerSeller (1..1) feature OptionFeature (0..1) observationTerms ObservationTerms (0..1) schedule CalculationSchedule (0..1) delivery AssetDeliveryInformation (0..1) underlier Underlier (1..1) optionType OptionTypeEnum (0..1) exerciseTerms ExerciseTerms (1..1) strike OptionStrike (0..1)

Like InterestRatePayout and CreditDefaultPayout, OptionPayout extends PayoutBase and inherits payerReceiver, priceQuantity, settlementTerms, and principalPayment. Above that, it adds nine attributes of its own. Two are mandatory: buyerSeller and exerciseTerms. One anchors the economics: underlier.

Nine attributes. Each answers a different question.

buyerSeller is mandatory (1..1). Unlike a swap where both parties have mutual obligations, an option is asymmetric: one party holds the right, the other bears the obligation. BuyerSeller captures this with buyer (pays premium, holds the right) and seller (receives premium, bears the obligation).

underlier is mandatory (1..1). It is a choice: Observable (an asset, basket, or index) or Product (a TransferableProduct or NonTransferableProduct). This is why OptionPayout can wrap anything — an equity, an FX rate, a commodity, a swap, a CDS. The type of the underlier determines the type of the option.

exerciseTerms is mandatory (1..1). It defines the exercise window: European (single date), Bermuda (multiple dates), or American (continuous). Without it, you don’t know when the right can be exercised.

strike is optional (0..1). A no-strike option is possible for certain structures. When present, it can be a price, a spread reference (CDS options), a swap curve reference (convertible bonds), or an averaging strike (Asian options). The four forms are mutually exclusive — a one-of condition enforces this.

optionType is optional (0..1). Put or Call for equity/FX/commodity options. Payer or Receiver for swaptions and CDS options. Straddle for strategies combining both.

feature is optional (0..1). It adds exotic overlays: barrier (knock-in/knock-out), Asian averaging, quanto FX conversion, dividend pass-through. None are required for a plain vanilla option.

observationTerms is optional (0..1). It defines how the underlier price is observed: time of day, information source, precision, and the schedule of observation dates. Relevant for Asian options and any option where the valuation depends on observed prices over a period rather than a single fixing.

schedule is optional (0..1). It provides a non-parametric way to define the payout schedule — specifying periods, quantities, and pricing data directly as explicit dates and values, rather than through parametric rules like a frequency and a roll convention. Used when the option has a complex or irregular schedule that cannot be expressed parametrically.

delivery is optional (0..1). It carries the physical delivery details — location, delivery capacity, delivery periods — for commodity options and other physically-settled options where the underlying asset must be transported or transferred, not just cash-settled.

Economic Agreement — On What, at What Strike, in Which Direction?

The economic core of an option is: what right is being bought, and at what price does it become valuable?

Direction: buyerSeller replaces PayerReceiver. The buyer pays the premium and holds the right. The seller receives the premium and bears the obligation if exercise occurs. This is a fundamentally different economic relationship from a swap. In a swap, both parties have payment obligations from inception. In an option, only the premium leg involves a certain payment. The exercise leg is conditional on the holder’s decision.

Underlier: underlier defines what the option is written on. For our swaption:

underlier: Product { TransferableProduct { economicTerms: EconomicTerms { payout: [ InterestRatePayout { // fixed leg: 3.50% payerReceiver: PayerReceiver { payer: Party2, receiver: Party1 } rateSpecification: FixedRateSpecification { rateSchedule: { value: 0.035 } } }, InterestRatePayout { // floating leg: 3M SOFR payerReceiver: PayerReceiver { payer: Party1, receiver: Party2 } rateSpecification: FloatingRateSpecification { rateOption: SOFR, indexTenor: 3M } } ] } }}

The underlier contains a complete, executable IRS definition. On exercise, this product becomes a live trade. The OptionPayout does not need to re-specify schedules, day counts, or settlement terms — they are already defined inside the underlier.

Strike: strike defines the level at which exercise is in the money. For our swaption, strikePrice: 0.035 means the holder has the right to receive 3.50% fixed. If the market swap rate at expiry is 3.00%, the option is in the money — the holder can receive 3.50% when the market would only pay 3.00%.

For a CDS option, the strike is not a rate but a spread, captured through strikeReference: FixedRateSpecification. For a convertible bond, the strike references a swap curve via referenceSwapCurve. The three forms are mutually exclusive because they serve different product types. One type. Different strike expressions.

Contractual Definition — When May the Holder Act?

Where InterestRatePayout fills Stage 2 with CalculationPeriodDates, PaymentDates, and ResetDates, OptionPayout fills it with exerciseTerms:

ExerciseTerms { style: European expirationDate: AdjustableOrRelativeDate { adjustableDate: AdjustableDate { unadjustedDate: 2027-03-15 } } expirationTime: BusinessCenterTime { hour: 11, minute: 0, businessCenter: USNY } expirationTimeType: Close relevantUnderlyingDate: AdjustableOrRelativeDates { adjustableDate: AdjustableDate { unadjustedDate: 2027-03-15 } }}

style — European: single exercise date, six months forward. If this were a Bermuda swaption, exerciseDates would list the specific dates. If an American equity option, commencementDate and expirationDate would bracket the continuous window.

expirationDate — 15 March 2027. If the holder has not exercised by 11:00 AM New York time on this date, the right expires. The expirationTime and expirationTimeType capture the precise cutoff.

relevantUnderlyingDate — 15 March 2027. This is the effective date of the underlying swap if exercised. It is not the same as the expiration date of the option itself, though they often align for European swaptions. For an FX option, this would be the value date for settlement of the underlying FX transaction.

partialExercise — allows the holder to exercise on less than the full notional. A holder of a USD 100M swaption might exercise on only USD 50M if they only need to hedge half the exposure.

Value Determination — Is the Option in the Money?

Value determination for an option is not formulaic in the way InterestRatePayout is. There is no dayCountFraction, no forecastAmount. Instead, it is a comparison:

Payoff = max(Underlier Value − Strike, 0) × Notional (for a call) Payoff = max(Strike − Underlier Value, 0) × Notional (for a put)

For our receiver swaption: the holder receives fixed 3.50% and pays 3M SOFR. At expiry, if the market swap rate for the remaining 5 years is 3.00%, the option is in the money. The holder exercises, entering into a swap where they receive 3.50% when the market would only give them 3.00%. The value is the present value of that 50bp annuity over 5 years on USD 100M.

For options where the underlier is an Observable, observationTerms defines how the underlier price is determined. For an Asian option, it specifies the averaging dates and methodology. For a barrier option, it defines the monitoring period — has the barrier been breached?

For our European swaption, no observation terms are needed. The market swap rate at the single expiration date determines the payoff. The model captures this through the style: European and the single expirationDate — no averaging, no continuous monitoring, no multiple observations.

Settlement / Realisation — What Happens on Exercise?

When the holder exercises, settlement follows one of two paths, both modelled through the inherited SettlementTerms:

Physical settlement — the underlier product is created. For a swaption, the IRS definition inside the underlier becomes a live trade between the two parties as of the relevantUnderlyingDate. The parties begin exchanging payments according to the swap’s schedules. Nothing is paid at exercise except any exerciseFee.

Cash settlement — the option pays the difference between the strike and the market value. For an equity call, if the stock is at USD 165 and the strike is USD 150, the seller pays USD 15 per share. No shares change hands. CashSettlementTerms on the inherited settlementTerms carries the valuation date and method.

For our swaption, the settlement is physical. On exercise, the underlying swap becomes effective:

settlementTerms: SettlementTerms { settlementType: Physical physicalSettlementTerms: PhysicalSettlementTerms { clearedPhysicalSettlement: true // if the swaption clears through a CCP }}

The CDM also carries a validation rule specific to swaptions: if physicalSettlementTerms exists and the underlier is a product with exactly two InterestRatePayouts (i.e., a swap), then clearedPhysicalSettlement must be specified — indicating whether the resulting swap will be cleared.

Conclusion

We have now seen three extensions of PayoutBase:

| Payout type | Extends PayoutBase with… | Economic logic |

|---|---|---|

InterestRatePayout | RateSpecification, schedules, dayCountFraction, compoundingMethod, DiscountingMethod | Scheduled interest-based obligation |

CreditDefaultPayout | GeneralTerms, ProtectionTerms, TransactedPrice | Contingent credit-based obligation |

OptionPayout | BuyerSeller, Underlier, ExerciseTerms, OptionStrike | Conditional right |

And we have seen three compositional patterns:

- A vanilla IRS composes two

InterestRatePayouts— same type, opposite directions. - A CDS composes one

InterestRatePayoutand oneCreditDefaultPayout— different types, shared infrastructure. - A swaption composes one

OptionPayoutwhose underlier contains a full product definition with twoInterestRatePayouts— a wrapper around a pre-defined composition.

OptionPayout is unique among the three: it does not describe a payment. It describes the right to create one.