The previous articles traced two extensions of PayoutBase: InterestRatePayout (scheduled) and CreditDefaultPayout (contingent).

This article introduces a third: OptionPayout (conditional).

At its core, OptionPayout models a right, not an obligation. Someone holds the right to do something. Someone else bears the obligation if that right is exercised. The right may be exercised on a single date, on multiple dates, or continuously over a window. What is delivered on exercise may be cash, a security, or an entire financial product.

The Core Idea: Optionality Attached to Anything

InterestRatePayout answers: someone pays interest to someone else on a schedule. CreditDefaultPayout answers: someone compensates someone else if a credit event occurs. OptionPayout answers: someone may choose to buy, sell, or enter into something, at a specified price, within a specified window.

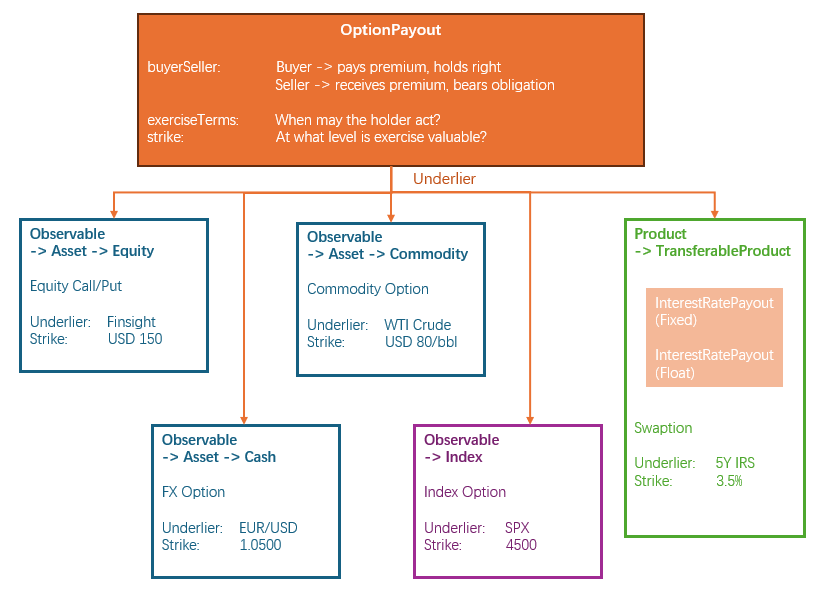

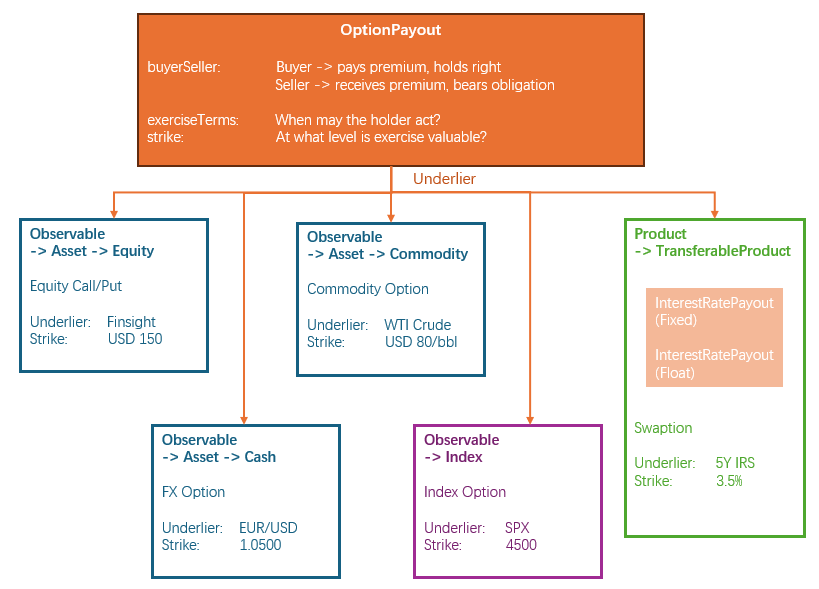

The key word is anything. The CDM designs OptionPayout so that the underlier — what the option is written on — can be any observable or any product:

choice Underlier: Observable // An asset (equity, bond, commodity), a basket, an index Product // A TransferableProduct or NonTransferableProduct

If the underlier is an Observable pointing to a stock, the option is an equity call. If it points to EUR/USD, it is an FX option. If it is a Product containing a full IRS definition, it is a swaption — and on exercise, that IRS springs into existence with all its schedules and settlement terms already defined.

The diagram below shows the same OptionPayout structure branching into five different product types depending only on what the underlier points to. The option logic stays the same. The underlier changes. The product changes.

The five branches are not five option types in the model. They are one type with different underliers.

Three Compositional Patterns

The underlier choice explains what the option is written on. But there is a second question: what structural role does the OptionPayout play in the product? Across all products, the answer is one of three patterns.

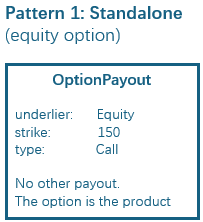

Standalone — the option IS the product. No other payouts. An equity call, an FX option, a commodity option.

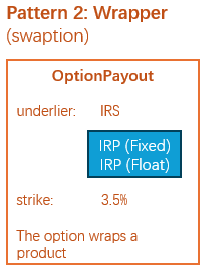

Wrapper — the option CREATES a product on exercise. The underlier contains a full product definition. A swaption, a CDS option.

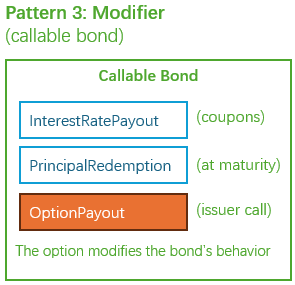

Modifier — the option sits alongside other payouts and CHANGES the product’s behaviour. A callable bond, a convertible bond, an extendible swap.

The rest of this article walks through each pattern with concrete product examples.

Direction: Buyer and Seller, Not Payer and Receiver

Where InterestRatePayout uses PayerReceiver (“who pays interest?”), OptionPayout uses BuyerSeller:

- Buyer — pays the premium, holds the right to exercise

- Seller — receives the premium, bears the obligation if exercised

This is a different economic relationship. In a swap, both parties have obligations. In an option, one party pays for a right and the other sells it. The direction is asymmetric from inception.

Product Examples

Standalone Options — The OptionPayout Is the Product

In these products, the option stands alone. There are no other payouts alongside it.

Equity option. A call on Finsight Tech Corp shares. Underlier is an Observable pointing to the equity. Strike is USD 150. OptionType is Call. Exercise is European — single date, three months forward. The holder pays a premium. If Finsight trades above 150 at expiry, the seller pays the difference. If not, the option expires worthless. One OptionPayout. No other payouts.

FX option. A EUR call / USD put. Underlier is an Observable pointing to EUR/USD. Strike is 1.0500. OptionType is Call. The holder has the right to buy EUR at 1.0500. Used by corporates hedging foreign currency exposure and by speculators.

Commodity option. A call on WTI crude oil futures. Underlier is an Observable pointing to the commodity. Strike is USD 80/barrel. Exercise may be American — the holder can exercise at any point before expiry, which matters when the underlying is physical and delivery logistics are involved.

Interest rate cap. A borrower buys a cap to limit floating-rate exposure. Each caplet is effectively a separate OptionPayout — if 3M SOFR exceeds 5.00% in a given period, the seller pays the difference. The underlier is an interest rate index. The strike is the cap rate. The option is exercised automatically if the rate is above the strike on the fixing date.

Digital option. A binary payout: if the underlier is above the strike at expiry, the seller pays a fixed amount. No proportional payoff — all or nothing. Same OptionPayout structure, different settlement logic.

Swaptions — The Underlier Is a Product

In these products, exercising the option does not produce a cash payment. It creates a whole new trade.

Interest rate swaption. The buyer pays a premium for the right to enter into a 5-year USD IRS, paying fixed 3.50% and receiving 3M SOFR, starting in six months. The underlier is a Product containing two fully-defined InterestRatePayouts. On exercise, those payouts become a live trade with all their schedules, day count conventions, and settlement terms already specified. The swaption is a wrapper around a pre-defined swap.

CDS index option. The buyer pays a premium for the right to buy or sell protection on CDX.NA.IG at a specified spread. The underlier is a Product containing a full CDS definition — one InterestRatePayout for the premium leg, one CreditDefaultPayout for the protection leg. On exercise, the buyer enters into the CDS at the strike spread. If the market spread has moved, the option is in the money.

Embedded Options — The OptionPayout Modifies Another Product

These are not standalone. The option sits alongside other payouts and changes the behaviour of the product it is embedded in.

Callable bond. A bond with three components: InterestRatePayout (periodic fixed coupons), PrincipalRedemption (face value at maturity), and OptionPayout (issuer’s right to call the bond early). The issuer may redeem the bond at par on specified call dates. From the bondholder’s perspective, this is a long bond position plus a short call option. The coupon is typically higher than a non-callable bond to compensate for the call risk.

Putable bond. The reverse: the investor holds the right to put the bond back to the issuer at par on specified dates. A long bond plus a long put option.

Convertible bond. The bondholder holds the right to convert the bond into a specified number of the issuer’s shares. The underlier is the equity. The strike is typically expressed via a referenceSwapCurve rather than a simple strike price. If the share price rises enough, conversion becomes more valuable than holding the bond to maturity.

Callable swap. A corporate enters into a 10-year IRS to hedge floating-rate debt. If rates fall, the corporate may want to refinance. The callable swap gives the corporate the right to cancel the swap early on specified dates. The swap itself is two InterestRatePayouts. The OptionPayout sits alongside them as a termination right.

Extendible swap. The reverse of callable: one party holds the right to extend the swap beyond its scheduled termination date. If rates are favourable, extend. If not, let it mature.

Exotics — The Feature Layer

The CDM models exotic option features through OptionFeature, an optional attribute on OptionPayout. These features modify the standard option payoff without changing the core structure.

Barrier option. A knock-out call on Finsight Tech Corp at USD 150, but with a barrier at USD 130. If the stock ever trades at or below 130 before expiry, the option is cancelled — even if it later finishes in the money. A knock-in works in reverse: the option only activates if the barrier is breached. OptionFeature.barrier captures the barrier level, the monitoring period, and whether it is knock-in or knock-out.

Asian option. The payoff depends not on the spot price at expiry but on the average price over the observation period. This protects against manipulation of the closing price on a single day and is common in commodities and FX. OptionFeature.averagingFeature defines how the average is computed.

Quanto option. The underlier is denominated in one currency (e.g., Nikkei 225 in JPY) but the payout is in another (USD). The option removes FX risk for the buyer. OptionFeature.fxFeature captures the conversion rate and methodology.

These features are optional layers on top of the base option structure. A plain vanilla option uses none of them. A barrier option uses one. A quanto Asian option might use three. You can view them as pluggable additions — the base structure stays the same, and features are attached as needed.

Structured Products — Composition at Scale

Equity-linked note. An investor buys a note that pays a coupon (an InterestRatePayout) and redeems at maturity based on the performance of an equity index (an embedded OptionPayout on the index). If the index rises, the investor participates in the upside. If it falls, the investor gets the principal back (or a portion of it). The product is composed of a bond plus a call option on the index.

Why Anything Can Be an Underlier

The CDM’s choice of Observable or Product as the underlier types is a deliberate design decision. It means:

- An option on a single stock uses

Observable → Asset → Instrument → Security - An option on a basket uses

Observable → Basket - An option on an index uses

Observable → Index - An option on a swap uses

Product → TransferableProduct → EconomicTerms → two InterestRatePayouts - An option on a CDS uses

Product → TransferableProduct → EconomicTerms → InterestRatePayout + CreditDefaultPayout

The type of the underlier determines the type of the option. The OptionPayout itself stays the same. The buyer pays a premium. The seller bears the obligation. The exercise terms define when. The strike defines at what level. The underlier defines on what.

That is composition — not by creating a separate option type per asset class, but by making the underlier a choice that can point to anything.

In the next article, I will walk through the OptionPayout type structure using the F-PAL framework — from economic agreement through to exercise and settlement.