The previous articles traced three extensions of PayoutBase, InterestRatePayout (scheduled), CreditDefaultPayout (contingent), and OptionPayout (conditional).

This article covers the fourth and simplest: SettlementPayout (deterministic).

At its core, SettlementPayout models a forward commitment. Two parties agree today to exchange one thing for another at a fixed price on a future date. Both are obligated. Neither has a choice. No schedule. No contingency. No optionality. Just: what, how much, at what price, on what date.

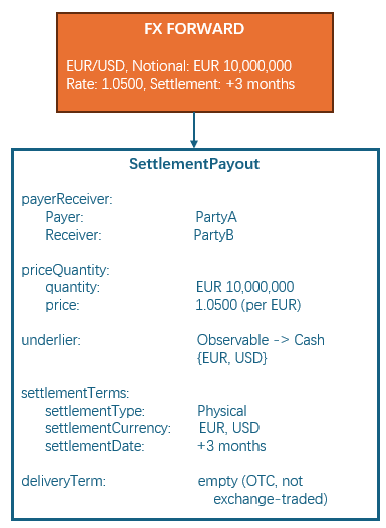

An FX forward on EUR/USD will serve as the running example: Party A buys EUR 10,000,000 from Party B at 1.0500, settling in three months.

A single payout. No companion leg. The exchange is embedded in the payout itself through the PayerReceiver and the priceQuantity pair — one party delivers one currency, the other party delivers the other. This is different from an IRS, where two InterestRatePayouts represent two separate payment streams. Here, the exchange is a single transaction.

SettlementPayout — The Type Structure

Four direct attributes, plus everything inherited from PayoutBase: payerReceiver, priceQuantity, settlementTerms, principalPayment. The smallest type surface of the four.

type SettlementPayout extends PayoutBase: underlier Underlier (1..1) deliveryTerm string (0..1) delivery AssetDeliveryInformation (0..1) schedule CalculationSchedule (0..1)

underlier is mandatory (1..1). Same choice type used by OptionPayout — Observable or Product — but with one restriction: the underlier cannot be a NonTransferableProduct. Settlement implies delivery, and a non-transferable product cannot be delivered. If the underlier is an Index, settlement must be cash — you cannot physically deliver the S&P 500. The CDM enforces both constraints as conditions on the type.

deliveryTerm is optional (0..1). For exchange-traded contracts, this is the standard contract identifier — “Z23” for December 2023, “H24” for March 2024. It follows exchange conventions, not calendar dates, because the delivery period for a futures contract has specific meaning defined by the exchange. For OTC forwards like our EUR/USD example, it is empty.

delivery is optional (0..1). Physical delivery details — location, capacity, periods. Shared with OptionPayout and CommodityPayout. Populated for commodity forwards where the grade, warehouse, and delivery window matter. Absent for cash-settled forwards and most FX forwards.

schedule is optional (0..1). A non-parametric way to define complex or irregular settlement patterns by specifying dates, quantities, and prices directly. Used when the settlement cannot be expressed as a single date or a simple parametric rule. Same type used by OptionPayout.

Product Examples

SettlementPayout appears in products where the economic structure is a single forward exchange. The underlier type determines the product — same pattern as OptionPayout.

FX Forwards and Spot

The most common use. The underlier is Observable → Asset → Cash representing a currency pair.

FX forward. Party A agrees to buy EUR 10,000,000 from Party B at 1.0500 USD/EUR, settling in three months. Both parties are obligated. One SettlementPayout. On the settlement date, Party A delivers USD 10,500,000 and Party B delivers EUR 10,000,000.

FX spot. Structurally identical to the forward, but the settlement date is T+2 (or T+1 for USD/CAD, T+0 for same-day). The CDM does not distinguish spot from forward — both use SettlementPayout. The settlement date tells you which one it is.

Non-deliverable forward (NDF). An FX forward on a restricted currency such as KRW or BRL. The underlier is still Observable → Asset → Cash { USD, KRW }, but settlementType = Cash. On the fixing date, the spot rate is observed. The difference between the agreed forward rate and the spot fixing is paid in the deliverable currency (USD). The restricted currency never moves. Some NDF structures also include an InterestRatePayout to represent the implied interest differential, making them two-payout products — one SettlementPayout for the FX settlement, one InterestRatePayout for the rate component.

Equity Forwards

The underlier is Observable → Asset → Instrument → Security pointing to a specific stock.

Equity forward. Party A agrees to buy 100,000 shares of Finsight Tech Corp from Party B at USD 150 per share, settling in six months. Party A pays USD 15,000,000. Party B delivers the shares. Both are obligated regardless of where the stock trades at maturity. Used for hedging, financing, and synthetic exposure.

Bond Forwards

The underlier is Observable → Asset → Instrument → Security pointing to a specific bond.

Bond forward. Party A agrees to buy USD 10,000,000 face value of the US Treasury 4.00% due 2030 from Party B at a clean price of 98.50, settling in one month. On settlement, Party A pays the full (dirty) price and Party B delivers the bonds. Used by dealers to position for rate moves and by funds to manage duration exposure.

Commodity Forwards

The underlier is Observable → Asset → Commodity. The delivery attribute carries the grade, location, and delivery window.

Commodity forward. A refiner agrees to buy 50,000 barrels of WTI crude oil at USD 80 per barrel, physical delivery to Cushing, Oklahoma, in December 2026. The deliveryTerm may carry “Z26” if the contract follows exchange conventions. The delivery attribute specifies Cushing as the delivery point. Unlike an FX forward, the physical delivery logistics matter — grade, location, and delivery schedule are part of the contract.

Index Forwards

The underlier is Observable → Index. The CDM enforces cash settlement only — you cannot physically deliver the S&P 500.

Index forward. Party A agrees to pay Party B the difference between the S&P 500 level at maturity and an agreed forward level of 4,500, multiplied by USD 100 per point. If the index is at 4,600, Party B pays Party A USD 10,000. Settlement is cash. No securities change hands.

Economic Agreement — What Is Being Exchanged?

The economic core of a forward is the simplest of the four payouts. There is no rate to determine. No credit event to define. No strike to compare against a market price. There is only: what is being bought, at what price, in what quantity.

underlier defines what. For our FX forward: Observable → Asset → Cash { EUR, USD }. The observable carries the currency pair — one leg of the exchange. The priceQuantity carries the rate (1.0500 USD per EUR) and the quantity (EUR 10,000,000).

For a commodity forward on WTI crude: Observable → Asset → Commodity { WTI Crude Oil }. The priceQuantity carries the price per barrel and the quantity in barrels. The delivery attribute carries the delivery location — Cushing, Oklahoma.

For an equity forward on Finsight Tech Corp: Observable → Asset → Instrument → Security { Finsight }. The priceQuantity carries the price per share and the number of shares.

For an index forward on the S&P 500: Observable → Index { SPX }. The priceQuantity carries the index level and the multiplier. Settlement must be cash — the CDM enforces this because you cannot deliver an index.

The same type. Four different asset classes. The underlier determines what is traded. The payout structure stays the same.

Contractual Definition — When Does Settlement Occur?

SettlementPayout has no CalculationPeriodDates, no PaymentDates, no ResetDates. It has a single settlement date, inherited from PayoutBase through settlementTerms:

settlementTerms: SettlementTerms { settlementType: Physical settlementCurrency: EUR, USD settlementDate: SettlementDate { adjustableDate: AdjustableDate { unadjustedDate: 2026-09-15 } }}

For an FX spot, the settlement date is T+2. For an FX forward, it is a date three months forward. For an exchange-traded future, it is defined by the exchange’s delivery calendar and identified by the deliveryTerm. The structure does not change. The date does.

Value Determination — The Simplest Case

Value determination for a forward is not a calculation. There is no dayCountFraction, no compoundingMethod, no forecastAmount. The price was fixed at trade inception. The amount is known.

The forward’s value changes over time as the market price moves — but that is a mark-to-market or valuation concern, not a payout calculation concern. The payout itself has nothing to compute at maturity. Party A delivers one currency. Party B delivers the other. The amounts were agreed on day one.

This is what makes SettlementPayout structurally simpler than the other three types. InterestRatePayout needs to observe rates and compute amounts. CreditDefaultPayout needs to determine recovery. OptionPayout needs to compare the underlier to the strike. SettlementPayout just settles what was agreed.

Settlement / Realisation — Physical or Cash

SettlementPayout inherits settlementTerms from PayoutBase, which supports both physical and cash settlement.

Physical settlement — the parties exchange the underlier. In an FX forward, Party A delivers USD 10,500,000 and Party B delivers EUR 10,000,000. In a commodity forward, the seller delivers barrels of WTI to Cushing and the buyer pays the agreed price.

Cash settlement — the difference is paid. In an NDF (non-deliverable forward) on a restricted currency like KRW, the underlier is still an Observable → Cash { USD, KRW }, but settlementType = Cash. On the settlement date, the fixing rate is observed and the difference between the agreed forward rate and the spot fixing is paid in the deliverable currency (usually USD). The KRW never moves.

Index forwards are always cash-settled — the CDM enforces this with a condition because an index cannot be physically delivered.

Conclusion

We have now seen four extensions of PayoutBase:

| Payout type | Extends PayoutBase with… | Economic logic |

|---|---|---|

InterestRatePayout | RateSpecification, schedules, dayCountFraction, compoundingMethod, DiscountingMethod | Scheduled interest-based obligation |

CreditDefaultPayout | GeneralTerms, ProtectionTerms, TransactedPrice | Contingent credit-based obligation |

OptionPayout | BuyerSeller, Underlier, ExerciseTerms, OptionStrike | Conditional right |

SettlementPayout | Underlier, deliveryTerm, delivery, schedule | Deterministic forward commitment |

SettlementPayout is the simplest because it has the least uncertainty. No rate to observe. No credit event to wait for. No decision to make. The model reflects this — four specific attributes versus ten for InterestRatePayout. The complexity is proportional to the uncertainty.