In the previous article, AI-Native Financial Data Foundation (5) – One IRS Example: From Product Nature to ISDA CDM Structure, I used a vanilla fixed-float interest rate swap as an overview example to show how a financial product can be decomposed into economic components.

That example naturally leads us to one of the most important concepts in the ISDA CDM product model: InterestRatePayout.

At first glance, InterestRatePayout may look like a technical object. It looks like one more type in a large data model. But from a business modelling perspective, it represents one of the most common economic patterns in FICC products: a scheduled accrual-style payment obligation based on notional, rate or spread, time period, calculation convention, and settlement rules.

In plain English, an InterestRatePayout answers a practical question:

Who pays whom, based on what notional, using what rate or spread logic, over what accrual period, on what payment date, and under what settlement rules?

That is already a lot of business meaning.

This is why InterestRatePayout deserves its own discussion. It is not just a field container. It is one of the core semantic building blocks for modelling interest-like payment economics across FICC products.

The Business Meaning of InterestRatePayout

An InterestRatePayout represents an economic obligation where the payment amount is determined by interest-rate-style accrual logic.

The simplest version of the idea can be expressed as:

Interest Amount = Notional x Rate x Day Count Fraction

For example:

USD 100,000,000 x 5.00% x 90 / 360 = USD 1,250,000

This formula is useful because it captures the basic intuition. Someone pays an amount based on a notional, a rate or spread, and a period of time.

It sounds very simple, isn’t? However, the simple formula is only the starting point. Real financial products are rarely that simple.

The notional may be fixed, amortising, accreting, resettable, FX-linked, or derived from another component. The rate or spread may be fixed, floating, inflation-linked, capped, floored, compounded, averaged, rounded, or subject to fallback rules. The day count fraction depends on calculation periods, calendars, business day conventions, and market conventions. The payment date may differ from the accrual end date. The settlement currency may differ from the notional currency. The product may or may not involve principal exchange.

This is the real business meaning of InterestRatePayout. It is not merely about calculating interest. It is about representing a scheduled accrual-style payment obligation in a form that can be decomposed, validated, projected, settled, and understood by systems.

Why InterestRatePayout Is Widely Reused

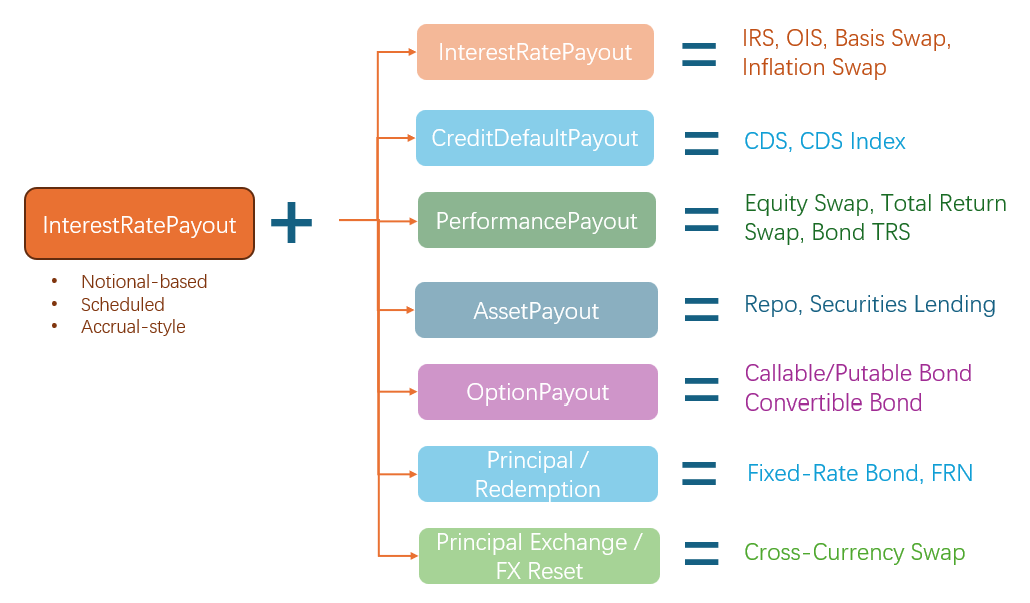

The reason InterestRatePayout is so widely reused is that many FICC products contain a scheduled, notional-based, accrual-style payment component.

Sometimes that component is a pure interest payment, as in an IRS, OIS, basis swap, or bond coupon. Sometimes it represents something slightly different, such as a CDS running premium, a repo financing charge, or the funding side of an equity swap. The underlying risk may be credit, funding, equity performance, collateral financing, or inflation, but the payment mechanics are still similar: notional, rate or spread, accrual period, schedule, and settlement.

This is why InterestRatePayout often acts as a stable component in product decomposition.

The other component then defines what makes the product special:

- another InterestRatePayout in an IRS or OIS

- CreditDefaultPayout in a CDS

- PerformancePayout in an equity swap or total return swap

- AssetPayout in a repo

- principal redemption in a bond or note

- embedded optionality in a callable or convertible bond

This does not mean products are mechanically invented by combining payout types. Real products come from market needs, legal documentation, risk transfer, funding requirements, regulation, and trading practice.

But from a modelling perspective, many products can be understood more clearly as compositions of reusable economic components.

That is the main point: InterestRatePayout gives us a stable way to model the scheduled accrual-style part of the product, while the other components explain the product-specific risk and behaviour.

A Compact View

| Product | InterestRatePayout role | Other component | Business implication |

|---|---|---|---|

| Vanilla fixed-float IRS | Fixed payout and floating payout | Another InterestRatePayout | Exchanges fixed-rate exposure for floating-rate exposure. |

| OIS | Fixed payout and overnight floating payout | Another InterestRatePayout | Exchanges fixed-rate exposure for overnight funding-rate exposure. |

| Basis swap | Floating payout on one index or tenor | Another floating InterestRatePayout | Transfers basis risk between two floating rate references. |

| FRA | Single-period interest payout | Net settlement logic | Represents a forward interest rate view over one future period. |

| Floating-rate note | Coupon stream | Principal redemption and security identity | Separates coupon economics from the full bond structure. |

| Fixed-rate bond | Fixed coupon stream | Principal redemption and security identity | Shows that bond coupons and swap payouts can share interest-based modelling ingredients. |

| Cross-currency swap | Interest payouts in different currencies | Principal exchange and FX-linked notional logic | Combines interest payments with cross-currency funding. |

| Inflation swap | Fixed or inflation-linked payout | Inflation index logic | Transfers inflation risk using an interest-rate-style structure. |

| CDS | Running premium stream | Credit protection payout | Combines scheduled premium payments with contingent credit protection. |

| Equity swap / TRS | Floating funding payout | Performance payout | Separates financing cost from asset return exposure. |

| Repo | Repo interest on cash | Securities transfer / collateral movement | Combines financing economics with asset movement. |

| Callable / convertible bond | Coupon stream | Embedded option | Coupon economics are interest-based, but behaviour depends on optionality. |

| Zero-coupon swap | Interest accrual with bullet payment | Another payout or settlement structure | Separates interest accrual from periodic cash payment. |

Interest Rate Swaps: InterestRatePayout plus InterestRatePayout

The cleanest example is the vanilla fixed-float interest rate swap.

A fixed-float IRS usually contains two InterestRatePayouts. One side pays a fixed rate, such as 3.50%. The other side pays a floating rate, such as 3M SOFR plus a spread.

The business meaning is an exchange of interest rate exposure. One party takes fixed-rate exposure, while the other takes floating-rate exposure. The product label is IRS, but the actual economic structure is two interest-based payment obligations pointing in opposite directions.

The same idea appears in OIS and basis swaps. In an OIS, the floating side references compounded or averaged overnight rates such as SOFR or SONIA. In a basis swap, both sides may be floating, but they reference different tenors, indices, or spreads. The product variation comes from the rate logic, reset rules, and schedule, not from abandoning the InterestRatePayout concept.

This is the first important lesson: many interest rate products are not fundamentally different at the component level. They are different configurations of InterestRatePayout.

FRA: A Single-Period InterestRatePayout

A forward rate agreement is useful because it breaks the mental link between InterestRatePayout and a long recurring swap stream. An FRA is usually a single-period product. The parties agree today on an interest rate for a future period, and settlement reflects the difference between the agreed rate and the market rate.

The business meaning is still interest-rate based. There is a notional, a forward accrual period, a fixed agreed rate, a reference floating rate, and a settlement amount.

So an InterestRatePayout does not always have to look like a multi-period swap stream. It can also represent a single-period interest-based obligation. This matters for modelling because the model should not assume that every interest-based payout has the same payment pattern.

Bonds and FRNs: InterestRatePayout plus Principal Redemption

Floating-rate notes and fixed-rate bonds show that InterestRatePayout concepts are not limited to derivatives.

A floating-rate note coupon may reference 3M EURIBOR plus 75 basis points, or SOFR compounded in arrears plus a spread. The coupon stream has the familiar ingredients of an interest-based payout: notional, rate index, spread, accrual period, day count convention, and payment date.

A fixed-rate bond coupon has a similar pattern, except the rate is fixed.

However, the whole bond is not just an InterestRatePayout. A bond has an issuer, security identity, maturity, principal redemption, and legal structure. InterestRatePayout explains the coupon economics, but not the whole security.

The business implication is important. A coupon stream and a swap payout may share modelling ingredients, but they belong to different product structures. Component-based modelling lets us recognise the shared economic pattern without confusing the products.

Cross-Currency Swap: InterestRatePayout plus Currency and Principal Logic

A cross-currency swap usually contains interest payouts in different currencies. For example, one party may pay USD SOFR on a USD notional, while the other pays EURIBOR on a EUR notional.

But a cross-currency swap is not only about interest payments. It may also involve initial principal exchange, final re-exchange, and sometimes notional reset based on FX observations.

This is where the product becomes richer. InterestRatePayout still captures the recurring interest-based obligations, but other components are needed to represent currency exchange, principal movement, and FX-linked notional behaviour.

The business implication is that InterestRatePayout can remain a stable component while the surrounding product structure becomes more complex.

CDS: InterestRatePayout plus Credit Protection

A credit default swap is not an interest rate product. It is a credit product.

However, the running premium stream paid by the protection buyer is periodic, notional-based, spread-based, and schedule-based. From a payment-structure perspective, it has interest-rate-style mechanics.

The other side of the CDS is completely different. It is not scheduled interest. It is contingent credit protection, triggered by a credit event and settled according to the contract.

This creates a clean asymmetric structure:

InterestRatePayout plus CreditDefaultPayout.

The business implication is that the product combines two different economic logics. One side is scheduled and accrual-based. The other side is event-driven and contingent.

This is a very useful example for AI-native modelling, because the product should not be understood only as “CDS”. It should be understood as a composition of premium payment economics and credit protection economics.

Equity Swap and Total Return Swap: InterestRatePayout plus Performance

In an equity swap or total return swap, one side often references the performance of an asset, index, or basket. The other side is commonly a floating funding payment, such as SOFR plus a spread.

The funding side can be analysed as an InterestRatePayout. The return side is different. It is a performance-based payout.

The business implication is that one party receives exposure to the asset return, while the other receives financing compensation. InterestRatePayout represents the funding cost of carrying the exposure.

This is why InterestRatePayout appears even in products that are not labelled as interest rate products. It often provides the financing side of a cross-asset structure.

Repo: InterestRatePayout plus Asset Movement

A repo is another important example because it combines cash financing with securities movement.

The cash side earns or pays a repo rate. That part has interest-rate economics. The other side involves the transfer and return of securities as collateral.

So the product is not merely an interest rate product, and it is not merely an asset transfer. It is a financing structure that combines interest economics with collateral movement.

The business implication is that InterestRatePayout can represent the cost or return on cash, while another component represents the securities side. This makes repo a good example of why FICC modelling needs both financial semantics and asset movement semantics.

Callable and Convertible Bonds: InterestRatePayout plus Optionality

Callable, putable, and convertible bonds show another important pattern.

The coupon stream may be interest-based. It may look like a fixed or floating InterestRatePayout. But the product also contains an option-like feature.

In a callable bond, the issuer has the right to redeem the bond early. In a putable bond, the investor may have the right to sell it back. In a convertible bond, the investor may have the right to convert the bond into equity.

The business implication is that InterestRatePayout explains the coupon economics, but it does not explain the full product behaviour. The embedded option changes valuation, risk, and lifecycle behaviour.

This is why we should not treat InterestRatePayout as the whole product. It is a reusable component inside a richer structure.

Inflation and Zero-Coupon Structures: Specialised Interest Logic

Inflation swaps and zero-coupon swaps show that even within interest-based products, the payout logic can vary significantly.

In an inflation swap, one side may pay a fixed rate while the other side pays realised inflation based on an index such as CPI. The payout is still notional-based and schedule-based, but the rate logic is linked to inflation rather than a standard floating rate index.

In a zero-coupon swap, interest may accrue over time but be paid only once at maturity. This separates interest accrual from periodic cash payment.

The business implication is that InterestRatePayout is not just the simple formula:

Notional x Rate x Day Count Fraction.

It is a structure that can support different ways of defining rate logic, accrual, and payment behaviour.

Why This Matters for AI-Native Financial Data

These product examples show why InterestRatePayout is such an important modelling concept.

Across different products, it can represent different business roles: interest rate exchange in IRS, OIS, and basis swaps; coupon income in bonds and floating-rate notes; funding cost in equity swaps and total return swaps; running premium in CDS; cash financing in repo; and interest accrual in zero-coupon structures.

The surrounding product may be very different. It may involve credit protection, equity performance, asset transfer, principal redemption, FX reset, inflation linkage, or embedded optionality. But the scheduled accrual-style payment component remains recognisable.

This is exactly why component-based modelling is powerful. We do not need to model every product as a completely isolated object. We can decompose products into reusable economic components and then understand how those components combine.

For an AI-native financial data foundation, this is very important.

An AI agent should not only classify a trade by product label. It should understand which economic components are present, what each component means, and how they interact.

For example, it should understand that an IRS contains two interest-based payment obligations. It should understand that a CDS combines a scheduled premium stream with contingent credit protection. It should understand that an equity swap combines a funding component with a performance component. It should understand that a repo combines cash financing with securities movement.

That is much more useful than a flat product label.

It allows the AI to reason about the product, generate mappings more safely, explain the trade structure, and validate whether the economic components make sense.

Final Thought

InterestRatePayout may look like a technical CDM type, but it represents a fundamental business idea: a scheduled accrual-style payment obligation based on notional, rate or spread, time period, calculation convention, and settlement rules.

That obligation appears across many FICC products, sometimes as pure interest, sometimes as coupon income, funding cost, running premium, or repo financing.

In this article, I focused on the business meaning and product examples of InterestRatePayout. The goal was to show why InterestRatePayout is not just a technical CDM type, but a reusable economic component that appears across many FICC products.

In the next two articles, I will follow the F-PAL framework to analyse its attributes in more detail. Part 9 will focus on the first two stages: the economic core and the time structure. Part 10 will then continue with the remaining stages: calculation, settlement, projection, and validation.